Last month I had a great week in La Playitas training with old friends and new. One of the new friends had only taken up cycling in the past year but he was strong. He didn’t know his own strength as he dropped everyone on any reasonable pinch. On the bigger climbs though he didn’t have the stamina. On one particular occasion he’d been encouraged by everyone else to stick with me on one of the longer climbs. We were riding side by side, chatting but keeping a decent pace and pulling away from the group. At that point in my mind I’d decided I ride friendly all the way to the top, it would be a good chance to chat.

About halfway up we rounded this bend and could see the top. He’d clearly not been expecting it to be so far and commented on the distance with some words to the effect he didn’t think he could hold the pace. Something was triggered in my mind. Without a conscious thought I was off, upped the pace, didn’t look back (that shows weakness), after a corner I’d push even harder so when he rounded it he’d be even more demoralised. I don’t think he even put up a fight. It was a shallow victory but it made me laugh how these stupid little games are played, how I couldn’t help myself. Like when you work your butt off to catch some unknown rider ahead on a climb, steel yourself for a breezy hello as you pass and then curse yourself that you now can’t ease up for fear of the shame of being re-passed. It’s part of the fun of training with groups. None of these little races are serious, in fact half the time (and half the fun) is that half the people don’t even know it was a race till after. In the latter half of the ride the group discussed this topic and my new friend started to learn this game that cyclists play.

I’ve come a cropper doing this. Last July I was staying at Pyrenees Multisport and tagged along on a long ride with a group also staying there. I didn’t know any of them but right at the start of the first climb, Le Col de Mente, I set off like it was a 5-minute climb. This is my usual tactic if I’ve decided it’s a race, used many times on Epic Camp, go so hard at the start that most just give up. No one came with me but 5 minutes up Nathan had cruised back up to me and was sat on my wheel. I should have twigged at that point. Then after another 15 minutes or so he went by and off in to the distance. He was so much better than me. I’d been at my limit and he was just sat there on my wheel, chatting. I smiled; it’s nice to have it served right back to you like that sometimes. Over the coming days I got to know him better, a very talented athlete who ended the camp by annihilating the Col Des Ares TT record.

Back to La Playitas. Mid week we headed to the lighthouse to do some repeats and see the sunrise. We planned to do three repeats each getting quicker. My running was going well and I was determined to nail the final repeat. I was running with two others and on the second repeat I kept dropping off the pace and apparently working hard to get back on. Come the last repeat Robin went off very quick and Roger commented it was too quick. That was enough for me and I pushed on repeating in my head “you used to be a fell runner, you were superb at running uphill”. I got second to the top and was quick enough that to this day I reckon Jo still thinks Roger and I are making it up. It certainly created some banter during the day. Though never agreed it was clear to all three of us knew that it was a race. It won’t be so easy next year.

A year a go I was swim training with Rachel. She wasn’t swimming her best and we were doing some long repeats. Come the last one I sensed I might manage to lap her. I didn’t say anything, it would be easier if only I knew it was a race. I got nowhere near. She knew the unwritten rule: if there’s a chance the leader could catch the back marker then the final rep is an outright race. No way would she let me win that and she found a big final effort. This rule is learnt early. I currently train with some very talented youngsters and come that last rep if they’re getting even the slightest sniff of weakness there’s a flat out race to lap me. With these guys, on average, I lose.

Our third EverydayTraining camp is about start and we try to incorporate this fun side of competition by including several races. They add to the camp experience but it’s still the anonymous racing that can prove most fun and if only a subset even realise it’s a race beforehand even better.

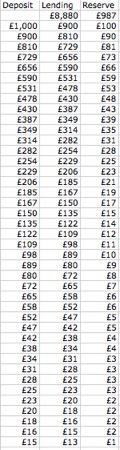

This chart illustrates what happens to a £1,000 deposit with a 10% reserve requirement. After 41 steps we’ve got lending of £8,880 and reserves of £987 sitting as deposits. The missing £13 is what was lent out at the last step which has not yet been deposited.

This chart illustrates what happens to a £1,000 deposit with a 10% reserve requirement. After 41 steps we’ve got lending of £8,880 and reserves of £987 sitting as deposits. The missing £13 is what was lent out at the last step which has not yet been deposited.