Do you ever think about where money comes from ? It’s not like people growing stuff, making stuff and selling it somehow produces money. Money is merely a method to allow us to facilitate trade. It needs to be created and put in to circulation. When it comes to hard cash it’s simple. The Royal Mint produces the stuff and sells it to the banks on behalf of the government. The money earned goes in to government coffers.

Ever wondered where the money comes from when you get a mortgage or borrow for a car ? Perhaps you believe that the money you are borrowing is someone else’s money who doesn’t need it right now.

According to CreditAction UK personal debt stands as £1,421,000,000,000. yes thats £1.421 TRILLION but I like to write it out fully so it hits home the completely insane number. Really do you think someone has got money sitting in a deposit account to that amount ? Ah but there’s fractional reserve banking you say. Yes there is. Banks realise that at any one time only a small amount of money that is deposited will ever be demanded so they only need to hold back a certain percentage of deposits and can lend out the rest. Since the money thats leant is spent and will ultimately end up as a deposit to which the same rule applies, you can lend a much higher percentage than the amount deposited.

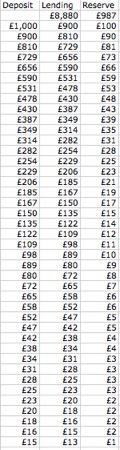

This chart illustrates what happens to a £1,000 deposit with a 10% reserve requirement. After 41 steps we’ve got lending of £8,880 and reserves of £987 sitting as deposits. The missing £13 is what was lent out at the last step which has not yet been deposited.

This chart illustrates what happens to a £1,000 deposit with a 10% reserve requirement. After 41 steps we’ve got lending of £8,880 and reserves of £987 sitting as deposits. The missing £13 is what was lent out at the last step which has not yet been deposited.

The formula for this is:

£Total Lending = (£Deposit – (Reserve% x £Deposit)) / Reserve%

Lets look at some figures:

UK National Debt: £1,278,200,000,000 (see here)

UK Personal Debt: £1,421,000,000,000 (as per above)

Total: £2,6999,200,000,000

Here’s the levels of deposits in £sterling required to support that given the above model:

At a 10% reserve requirement a mere £299,911,111,111 of deposits (yes 300 BILLION)

At a 3% reserve requirement it’s down to £83,480,412,371 of deposits

Even at 3% do you imagine that there are people out there that together have got £83 billion sitting in savings accounts.

If you’re confused don’t worry, I reckon even most economic graduates don’t understand how this really works. I did economics a-level and worked in Interest Rates in a bank for over 15 years and it wasn’t till I left the bank and studied it independently that I figured it out. So please stick with this as it’s important people understand.

Here’s what actually happens when you get a loan from the bank. Once they agree your loan they make a double entry in their accounts (yes I trained as a chartered accountant before going a bank). The following:

- In you nominated account they add the money you’ve borrowed. This is money they owe you (i.e. you can spend it)

- They create an asset on their balance sheet the money you owe them.

Thats it !! You head off and spend your money and they left with this asset. YES they have created money out of thin air. There is no longer a formal reserve percentage in the UK. There are some broad brush capital requirements for banks but when they lend they create money.

So how much money are the banks creating ? It’d be nice to know as it sounds like a bit of a money spinner – you create something more or less out of nothing (you need some book keeping) and then charge interest on it. Before I get on to this it’s worth while pointing out that the only reason this works, like any form of money, is because we all completely trust that payments can be made electronically and that if needs be we can convert this electronic money in to cash. More on this later.

Per the Bank of England site (look here )

They have broad money (~ cash + all deposit accounts) at £1,643,600,000,000

Narrow money (cash + BofE reserves) at £63,362,000,000 -> This is money the government creates

The narrow money is 3.86% of the total which means the private banks create over 94% of our money supply.

This should shock you. It’s important to pause here and just think of the implications.

- This means that 94% of all money is created from debt. i.e. when the money is created an equivalent amount of debt is create

- This means if you have £10,000 in a deposit account someone somewhere has nearly that amount of debt

- The banks are deciding where 94% of money created is allocated.

- This means if we pay off any debt the money disappears.

Read the last one again. So when politicians talk about paying off the debt it appears to me they really haven’t got a clue. If we managed to do that we would massively reduce the money supply which would bring about a massive depression.

The problem is it’s worse than this.

So the majority of our money is created by debt. Now when you borrow you have to pay back plus interest. Where is that interest going to come from ? Given all the cash is only 4% of the money supply there’s no way that money is paying back your interest. The only way the debt can be paid back is by more money being created. This means more debt has to be taken out to pay the original money back. I hope you see this is never ending. It’s why we HAVE TO HAVE GROWTH for our economic model to work. It’s also why the majority of the population is currently doomed to ever more debt. The knock on effect of this is something for another post.

The key thing to realise is that under this model it is IMPOSSIBLE to pay off the debt.

The second implication of this is that private banks are deciding where most money is allocated. Lets look at it from a banks point of view – where would you tend to lend ?

- To productive businesses where the risk is if they fail you get nothing back; OR

- To people buying houses where if they can’t pay you get most (possible all) your money back because of the asset

I’m hoping you see that B is going to be the preference.

I recently read a book about the Wiemar Republic and hyper inflation. At the time the government saw inflation and felt they had to keep printing money to allow people to buy stuff. It’s only after the fact people realised that it was the excessive printing of money that created the hyper inflation.

So with banks creating so much money why haven’t we had hyper inflation ? WE HAVE. Look at house prices. The inflation has come where they’ve allocated the money – thats been house prices and various speculative bubbles – think dot.com bubble, think sub prime bubble.

Given the key role private banks are playing in our money supply you can see why they are ‘Too Big To Fail’. The government puts in place the Financial Services Compensation Scheme to protect your deposits up to £85,000. This is very re-assuring for us as individuals but really it’s a pretty stupid thing to put in place. Basically the government is taking a huge chunk of risk from the banks. Why not take more risks when you know the government will pay out like this. Also, they know they’re too big to fail so why not risk a bit more.

For me the solution to the banking problem and the solution to the massive debt problem are one and the same. This power to create money has to be taken away from the banks and put in more responsible hands. There is precedent for this. This will be the topic for a future post.