PHLs prove a great success. Most people deposit their week of time and the money supply stabilises. Few see any need to redeem PHLs, instead they work for someone else to earn PHLs or have a business that sells something for PHLs. People tend to hold on to a few PHLs just in case. In time the idea of a PHL bank is put forward for the safe keeping of PHLs. The community feels it best for this to be separate from the Bank so they rename that the Central Bank and a new Peoples Bank is opened to take there deposits. Again the person running the bank is paid a salary by depositors for the safeguarding of their PHL deposits.

The owner of the peoples bank notices that most deposits remain untouched and comes up with a cunning idea. Rather than the depositors paying him to safeguard them he will instead safeguard them in return for being allowed to lend their money out. He earns by charging a fixed fee (say 1%) for lending out money. He agrees that a certain amount needs to be kept at the bank in case someone wants their PHLs. He calls this his ‘Reserve’ and decides to set it at 50%.

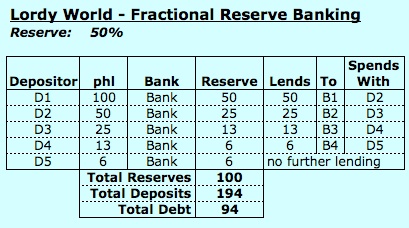

He lends out 50% of the deposits which gets spent and re-deposited with him. He can lend out 50% of this new deposit. Before long he’s lent out ever smaller amounts and hits the limit of his lending having more or less doubled the level of deposits. (see the table left that illustrates how this works). This means the people as a whole feel they have double the amount of money but in fact there is only the same number of PHLs (ie actual hours deposited). It means that if all of them tried to remove their money at the same time the bank has a big problem. Before I address this specific problem I’d like to illustrate how, in theory, this could unwind itself:

He lends out 50% of the deposits which gets spent and re-deposited with him. He can lend out 50% of this new deposit. Before long he’s lent out ever smaller amounts and hits the limit of his lending having more or less doubled the level of deposits. (see the table left that illustrates how this works). This means the people as a whole feel they have double the amount of money but in fact there is only the same number of PHLs (ie actual hours deposited). It means that if all of them tried to remove their money at the same time the bank has a big problem. Before I address this specific problem I’d like to illustrate how, in theory, this could unwind itself:

Looking at the chart all the borrowers could sell there products (which they borrowed to produce) for phl 100 to D1 (who removes his deposit to pay them – strictly speaking at this point the bank has broken it’s reserve requirement as all it’s reserves are gone but lets assume all the transaction happen in short order) allowing them to pay phl 1 to the banker (his fee), pay off all debts and make phl 5 profit. D1 would have zero deposit. There would be no debt. Leaving phl 94 deposits, phl 1 with banker and phl 5 with borrowers, totally phl 100 which is what we started with.

This shows how it can work, allowing people to get access to PHLs as they require. Soon, our, now two, bankers, realise that they could increase money circulation if they reduce the reserve requirement however the more they do this the more they run the risk of demands for deposits exceeding the reserves which could result in a run on the bank (loss of confidence) and in turn could bring down the whole system. The Bank can’t print money to address this BUT the Central Bank could especially as he’s realised that PHLs are hardly ever redeemed. He could help the Bank overcome any short term liquidity problems he has by simply printing more PHLs. He could work with a reserve he has to keep against redemptions. Provided this reserve is prudent enough he should be OK (say 50%). Lets walk through how this would work.

The Bank goes to 25% reserve which means he can lend out 3x the deposits he has which he does increasing the money supply to 400% of it’s original. He then finds that 30% of the deposits are demanded so he goes to the Central Bank who prints the extra 5%. Now there are more PHLs in circulation than hours deposited but as long as everyone doesn’t decide to redeem at once it’s ok. In short order the liquidity problem at the bank passes (eg deposits made, debt repaid, fees paid) and he can repay the money to the Central Bank plus his fee.

Again lets make some observations

- We now have hours somehow creating more hours. Since the bank lends out PHLs and gets those back plus a fixed fee. Where are those extra PHLs (hours) coming from ? The banker has done nothing of intrinsic value. He’s reliant on the borrower using the money to produce something she can sell for more PHLs than she borrowed.

- Growth is now needed by this system to pay of the debts. In this scenario have we had growth ? Here I mean in a more general sense (rather than increase in GDP). Say the borrower made something, for example a chair. At the end of the scenario there is still the same money in existence plus a chair which has some worth – hence the economy grew.

- Growth is limited provided it’s assessed as growth in overall wealth. Given the chair example once everyone has enough chairs thats it. If you measure growth based around money changing hands (as our financial system does) then if someone chucks out their chair and buys a new one that could contribute growth.

- Increased money supply is based on creation of credit. Lowering the Banks reserve requirement increases the amount of money available. Adjusting the fixed fee charged for credit can influence how much available credit is taken up.